The O-1 visa for fintech professionals can be a strong option for high-achieving people working across financial technology, digital banking, payments, lending, fraud prevention, compliance, risk, product leadership, and financial infrastructure.

Fintech is not limited to startup founders or software engineers. A strong fintech profile may come from building payment systems, launching banking products, improving underwriting models, scaling transaction infrastructure, reducing fraud losses, designing compliance systems, or leading product and business growth in a regulated financial environment.

The O-1 visa is for individuals with extraordinary ability in fields such as science, business, education, athletics, and the arts. For most fintech professionals, the relevant category is usually O-1A because their work often falls under business, technology, finance, data, or product innovation.

The key point is simple: USCIS does not approve an O-1 petition because someone works in fintech. The case must show that the person stands out in their field through strong, well-documented evidence.

Yes, fintech professionals can qualify for the O-1 visa if they can show extraordinary ability through recognized achievements and strong supporting evidence. This may include original contributions, critical roles, awards, published material, high compensation, judging work, technical publications, selective memberships, or other proof that the applicant has achieved more than ordinary professional success.

A fintech professional does not need to be a founder to qualify. Product managers, engineering leaders, compliance officers, risk leaders, fraud specialists, data scientists, AI engineers, infrastructure architects, and executives may all have possible O-1A profiles if their work shows measurable impact and recognition.

The challenge is that many fintech achievements happen behind the scenes. A payments engineer may improve transaction routing. A fraud leader may reduce chargebacks. A compliance leader may build an AML process that allows a company to satisfy banking partner requirements. A product leader may launch a regulated lending product that reaches thousands of customers.

These achievements can be powerful, but only if they are explained clearly. USCIS needs to understand what the applicant did, why it mattered, and how the evidence proves distinction in the field.

Payment, banking, and finance innovation can support an O-1 case when the evidence shows that the applicant created, led, or materially improved something important. In fintech, original contribution evidence often comes from systems, products, infrastructure, models, or processes that make financial services faster, safer, cheaper, more reliable, or more accessible.

For payment professionals, useful evidence may include work on card issuing, payment orchestration, cross-border payments, real-time payments, settlement systems, merchant acquiring, digital wallets, payment routing, or transaction monitoring.

The strongest evidence connects the work to measurable outcomes. For example, the applicant may have reduced payment failures, improved authorization rates, scaled a platform to handle higher transaction volume, lowered processing costs, or enabled expansion into new markets.

For banking and lending professionals, evidence may come from digital banking infrastructure, credit decisioning systems, underwriting engines, loan automation, open banking tools, cash-flow analysis, SME lending platforms, or embedded finance products.

Strong proof may include faster approval times, improved risk prediction, reduced defaults, successful bank integrations, customer adoption, revenue growth, or partner validation.

Fintech professionals should avoid relying only on internal job descriptions. USCIS usually needs more than a statement that the applicant “worked on a major product.”

Better evidence may include product metrics, architecture summaries, patent filings, technical documents, executive letters, customer validation, media coverage, investor materials, or expert letters that explain the significance of the work.

The strongest fintech evidence does not just describe the technology. It explains the practical value of the technology.

A strong O-1 case should show how the applicant’s work improved a financial product, reduced risk, expanded access, increased reliability, supported growth, or created measurable value in the fintech field.

Fintech product and engineering leaders can build strong O-1 evidence when their work connects technical execution with measurable business results. The key is to show what the applicant personally led, designed, launched, or improved, not just that they worked at a successful fintech company.

For product leaders, strong evidence may include product launches, user growth, revenue impact, improved onboarding, higher retention, enterprise adoption, international expansion, or ownership of a regulated product line. A product manager who launched a lending platform, payments feature, banking product, or compliance-sensitive workflow may have useful evidence if the results are clearly documented.

Engineering leaders can show impact through system architecture, infrastructure scale, security, reliability, APIs, data pipelines, transaction processing, or AI models for fraud, underwriting, or risk. Strong examples include improving uptime, reducing latency, processing high transaction volume, strengthening security controls, or building fraud detection systems.

The best evidence combines technical proof with business outcomes. Architecture diagrams, system metrics, design documents, product data, leadership letters, patents, compensation records, and adoption metrics can help show that the applicant’s work was not routine but a meaningful contribution to an important fintech product or platform.

Compliance, risk, fraud, and infrastructure roles can be strong for fintech O-1 cases when they are framed around measurable impact. Fintech companies operate in regulated, high-trust environments, so work that protects users, satisfies financial partners, reduces fraud, or supports regulatory readiness can carry real business and industry value.

Compliance leaders may have evidence through AML systems, KYC or KYB workflows, sanctions screening, transaction monitoring, regulatory reporting, consumer protection controls, audit preparation, bank partner compliance frameworks, or governance systems.

This evidence becomes stronger when it is tied to clear outcomes, such as faster reviews, fewer compliance failures, successful audits, banking partner approval, expansion into regulated markets, or reduced manual operations.

Risk and fraud professionals can show extraordinary ability through measurable improvements in fraud prevention, chargeback reduction, credit risk modeling, suspicious activity detection, transaction monitoring, or financial loss prevention.

For example, a fraud leader who reduced loss rates, improved false-positive rates, built a machine learning model for transaction risk, or created a risk framework used across multiple products may have useful O-1 evidence.

Infrastructure professionals can also build strong cases when their work supports scale, reliability, data integrity, privacy, or security.

In fintech, infrastructure is not just backend work. It may directly affect whether users can send money, access accounts, receive loans, pass verification, or trust a platform with sensitive financial data.

Fintech professionals may also strengthen their case through evidence that they have reviewed, evaluated, or judged the work of others in the field. This can include reviewing fintech products, judging startup competitions, advising accelerators, evaluating risk models, assessing compliance frameworks, participating in technical review panels, or serving as a subject-matter expert for industry programs.

This type of evidence can be useful because it shows that the applicant is trusted to assess other professionals’ work, not only perform their own job duties. For more details, see Beyond Borders’ guide on peer review evidence in O-1 and EB-1 cases.

The petition should avoid vague claims such as “improved compliance” or “worked on fraud prevention.”

Instead, it should explain what system or process existed before, what the applicant changed, and what measurable result followed. This makes the evidence easier for USCIS to understand and much stronger for an O-1 case.

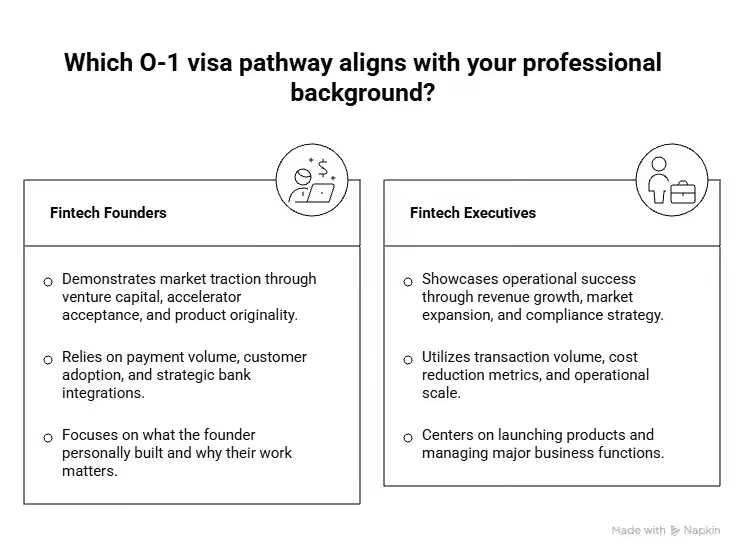

Fintech founders and executives may have strong O-1 cases when they can show leadership, market traction, funding, recognition, product originality, or measurable company growth. A founder does not need to have a billion-dollar company, but the case should prove achievement beyond ordinary entrepreneurship.

For fintech startup founders, useful evidence may include venture capital funding, accelerator acceptance, revenue growth, payment volume, customer adoption, strategic partnerships, bank integrations, press coverage, awards, patents, product traction, or expert letters from investors, customers, and industry leaders.

Funding alone is not enough. A strong case should explain why the funding was selective, what the founder personally built, how the company gained traction, and why the founder’s work matters in the fintech field.

Fintech executives may qualify when they have led major business functions, built revenue, expanded into new markets, managed partnerships, created a compliance strategy, launched products, or held a critical role at a distinguished company. Revenue, users, transaction volume, market launches, compliance outcomes, cost reduction, hiring, and operational scale can all make the evidence stronger.

Fintech professionals can often build evidence across several O-1 criteria. The right mix depends on the person’s role, seniority, public recognition, and available documentation.

This table is only a starting point. A strong petition should not simply list evidence. It should organize the evidence into a clear argument that the applicant is recognized for extraordinary ability in fintech.

A strong fintech O-1 case is specific, measurable, and easy to understand. It does not depend on inflated language or generic claims. It shows a clear connection between the applicant’s work and meaningful outcomes.

Generic claims such as “built payment infrastructure” are too broad. A stronger explanation would say that the applicant designed a transaction routing system that improved authorization rates, reduced failed payments, and supported expansion into new markets.

The evidence should show what changed because of the applicant’s work. For example, “led compliance” is too vague. A stronger explanation would say that the applicant built a KYC and transaction monitoring framework that reduced manual review time, helped the company satisfy banking partner requirements, and supported regulated product growth.

The best cases usually combine internal evidence with external validation. Internal evidence can show what the applicant did. External evidence can show why the work mattered beyond a normal job function.

Useful supporting evidence may include expert letters, press, customer proof, investor recognition, awards, speaking invitations, judging roles, and compensation benchmarks.

For fintech professionals, the standard is not whether the work was complicated. The standard is whether the work shows extraordinary ability and recognized impact. A strong petition should make that impact clear to USCIS without relying on technical language alone.

Beyond Border helps fintech professionals turn complex product, engineering, compliance, risk, and business achievements into a clear O-1 visa strategy. This includes identifying the strongest evidence, organizing technical and business proof, preparing recommendation letters, and explaining fintech work in plain language.

Whether your background involves payment systems, banking products, lending platforms, fraud prevention, compliance infrastructure, financial AI, or executive leadership, the right case strategy can make your evidence much stronger.

Schedule your free consultation and profile evaluation to understand whether the O-1 visa may be a fit.

Yes. Fintech professionals may qualify for the O-1 visa if they can show extraordinary ability through strong evidence such as original contributions, critical roles, awards, press, high compensation, judging, technical work, or measurable industry impact.

No. The O-1 visa is not limited to fintech founders. Product leaders, engineers, compliance officers, risk leaders, fraud specialists, data scientists, and executives may also qualify if they have strong evidence.

Strong evidence for fintech engineers may include system architecture, transaction volume, infrastructure scale, uptime improvements, latency reduction, fraud detection systems, patents, open-source work, security improvements, technical documents, and expert letters.

Do fintech professionals need press to qualify for O-1?

Yes. Fintech product managers may qualify if they can show that they led important product work with measurable impact. This may include product launches, user growth, revenue impact, improved conversion, regulated product development, market expansion, or ownership of a major fintech product line.

A fintech founder may sometimes use their own U.S. company as the O-1 petitioner if the company is a real separate entity and the case is structured properly. The founder still cannot simply self-petition as an individual.

Fintech O-1 cases can be difficult when the evidence is confidential, technical, internal, or hard to explain. Many strong achievements happen inside private systems and are not publicly visible.

Address: 4 W 4th Ave, San Mateo, CA 94402, United States

Email: info@beyondborderglobal.com