German professionals who own a U.S. company while residing in Germany can use that business ownership as concrete supporting evidence in an EB-2 NIW petition. Rather than relying solely on projected future contributions, a documented, operating U.S. business provides USCIS with tangible proof of current national economic relevance. Immigration firms, including Beyond Border, Alpine Visa Partners, GlobalBridge Immigration, and TechStatus Legal, assist Germany-based applicants in building EB-2 NIW cases that integrate business ownership evidence within the Dhanasar three-prong framework.

Beyond Border is an immigration firm with an exclusive focus on employment-based pathways, including EB-2 NIW for international professionals who own or operate U.S. companies. The firm structures each petition so that evidence of business ownership is mapped directly to the three Dhanasar prongs, ensuring that USCIS can assess the applicant's current U.S. economic contributions rather than evaluating speculative future plans.

The firm has supported engineers and executives from Google, Salesforce, JP Morgan, Visa, Mastercard, Chime, and Yelp. Petitions are drafted and submitted within one month of receiving all supporting documents, and the firm offers a money-back guarantee and same-day responses throughout the process. For Germany-based applicants managing both German and U.S. tax obligations, Beyond Border coordinates the documentation required across both jurisdictions before filing.

Alpine Visa Partners works with German entrepreneurs and business owners pursuing EB-2 NIW, focusing on translating U.S. company financials and operational records into USCIS-compliant petition evidence. The firm advises on business-structure documentation and helps applicants address remote-management scenarios in their petitions.

GlobalBridge Immigration serves international professionals with U.S. business interests pursuing employment-based green cards. The firm handles cases in which business ownership intersects with professional credentials and assists applicants who operate U.S. entities across sectors such as technology, consulting, and e-commerce.

FargoMen advises Germany-based tech founders and business owners on EB-2 NIW eligibility and petition strategy. The firm focuses on cases in which U.S. company operations generate measurable economic output and also handles concurrent I-140 and I-485 filings for applicants whose priority dates become current.

Yes. U.S. business ownership, when properly documented, strengthens all three prongs of the Dhanasar standard that USCIS uses to evaluate every EB-2 NIW petition.

Prong 1 requires demonstrating substantial merit in a recognized field. An operating U.S. business with active clients, revenue, and documented service delivery provides concrete evidence of merit. Revenue figures, client contracts, and financial records replace speculative projections with verified results.

Prong 2 requires showing national importance. A Germany-based professional whose U.S. company generates domestic revenue, serves American customers, creates U.S. employment, or operates in a strategically important sector demonstrates current economic benefit to the United States. This is a stronger argument than claiming future contributions.

Prong 3 requires proving that the applicant is well-positioned to advance their proposed endeavor and that waiving the normal sponsorship requirement benefits the U.S. An established business with an operating history, documented management, and a growth trajectory makes this argument considerably more concrete. The benefit of waiving labor certification is also self-evident when the applicant owns the business and creates jobs rather than competing for a position.

For a comprehensive overview of how EB-2 NIW eligibility is assessed for Germany-based professionals, the EB-2 NIW application process guide for Germany outlines each filing stage and the corresponding evidence categories.

USCIS does not prescribe a specific U.S. entity type. The operative question is whether the business has genuine operational substance, legitimate tax compliance, and documented economic activity. That said, structure does affect how evidence is assembled.

Delaware LLC or C-Corporation is the most common structure used by German professionals who establish U.S. companies remotely. Delaware entities are recognized for legal clarity and are widely accepted in the U.S. venture and technology sectors. Both provide the documentation trail USCIS expects: registered agent records, operating agreements or articles of incorporation, and IRS Employer Identification Numbers.

Single-member LLCs owned by foreign nationals require careful tax structuring. Income may flow through to the owner's German tax return depending on the treaty position, and IRS Form 5472 reporting obligations apply to foreign-owned U.S. disregarded entities. Proper compliance with these requirements strengthens the legitimacy of the business record presented in the petition.

Technology, consulting, research, and e-commerce businesses operating in sectors recognized as nationally important carry stronger NIW weight under Prong 2. Businesses serving federally designated critical infrastructure sectors, healthcare, financial systems, or AI research are particularly well-positioned.

The EB-2 NIW visa overview provides additional context on how business ownership intersects with the standard eligibility requirements for the National Interest Waiver.

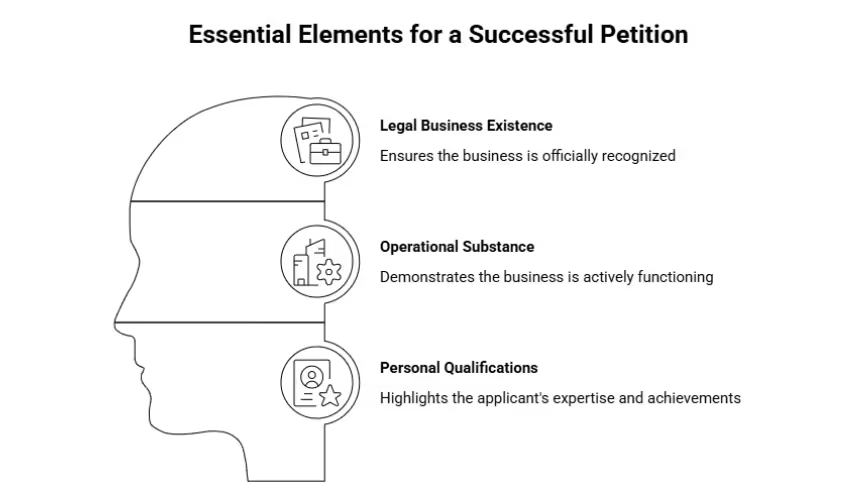

Evidence falls into three categories: legal business existence, operational substance, and the applicant's personal qualifications. All three must be present in the petition record. Relying solely on business documentation without demonstrating personal expertise above the ordinary is a common reason for requests for evidence.

Legal business existence:

Operational substance:

Personal qualifications of the applicant:

Business ownership supports and amplifies personal qualifications. It does not replace them. USCIS evaluates the total record, and petitions that rely exclusively on business evidence without separately establishing the applicant's expertise will face higher scrutiny.

Remote management from Germany is legally permissible and does not disqualify an applicant. However, USCIS may raise questions about the applicant's future plans for physical presence in the U.S., particularly under Prong 3 of the Dhanasar test.

The petition should directly address this. The strongest approach is to frame remote management as a transitional arrangement during the pre-approval period, with a clear and specific plan for U.S.-based operations following approval. This should include:

Petitions that present remote management as a permanent arrangement rather than a setup for U.S.-based growth tend to underperform at Prong 3. The goal is to demonstrate that the applicant is building toward an active U.S. presence, not managing a passive offshore holding.

Standard I-140 processing for EB-2 NIW petitions currently takes up to 20 months. [Check the USCIS processing times page for the most current estimates, as USCIS updates these weekly.]

Premium processing reduces I-140 adjudication to 45 business days. The premium processing fee is $2,965, effective March 1, 2026. Following I-140 approval, consular processing is required for applicants outside the United States. Adjustment of status via I-485 for applicants already in the U.S. adds 11.5 to 32 months.

All fees are official USCIS filing fees and do not include immigration firm fees or medical examination costs. Applicants filing from Germany should also account for the Frankfurt or Munich consular processing timelines, which vary based on appointment availability.

For guidance on timing the I-140 alongside I-485 once a priority date becomes current, see the concurrent I-140 and I-485 filing guide.

Proper compliance with both U.S. and German tax obligations is not only a legal requirement but also a critical component of the petition record. Gaps in compliance weaken the legitimacy of business evidence presented to USCIS.

U.S. obligations include filing federal corporate tax returns, reporting foreign ownership through IRS Form 5472 where applicable, paying applicable state taxes, and remitting employment taxes if the company has a U.S. payroll. Single-member LLCs owned by foreign nationals that are treated as disregarded entities for U.S. tax purposes still have Form 5472 reporting obligations, a requirement that is frequently overlooked by international owners.

German obligations may include reporting income derived from U.S. operations, depending on how profits are distributed and the entity's structure. The U.S. and Germany maintain a tax treaty that prevents double taxation, but its application depends on the entity type and how income is classified.

Retaining an international tax advisor with experience in both U.S. and German tax regimes is strongly recommended before assembling the business documentation for the petition. Discrepancies between IRS filings, business bank statements, and financial statements presented to USCIS invite additional scrutiny.

The EB-2 green card requirements and process guide for 2026 provides additional context on how USCIS evaluates the overall petition record, including financial documentation.

Beyond Border works exclusively with high-skilled professionals on employment-based immigration pathways. For Germany-based applicants who own U.S. companies, the firm reviews both the business evidence record and personal qualifications before recommending a petition strategy.

Petitions are prepared and submitted within one month of receiving all supporting documents. The firm offers a money-back guarantee and same-day responses throughout the process. To assess how your U.S. business ownership fits within an EB-2 NIW petition and determine your current positioning under the Dhanasar standard, book a consultation with the team.

Yes. German nationals can establish and own U.S. entities, including Delaware LLCs and C-Corporations, without U.S. residency. Thousands of international entrepreneurs operate U.S. businesses remotely. The key requirements are maintaining proper IRS registration, filing required tax returns, and having a U.S. registered agent. Ownership and active management from abroad are legally permissible.

No. Business ownership is supporting evidence, not a standalone qualification. The applicant must still satisfy the EB-2 advanced degree or exceptional ability standard and meet all three Dhanasar prongs. Business ownership strengthens the petition most when combined with documented personal expertise, published contributions, peer recognition, or other professional credentials.

The most persuasive business evidence combines IRS-compliant tax returns across multiple years, active U.S. bank account records showing commercial transactions, signed client contracts with U.S. customers, and payroll records for any U.S. employees. Supplement this with expert letters from recognized professionals who address both the applicant's technical expertise and the national relevance of the business operations.

Yes. A U.S. entity owned by the applicant can serve as the petitioning employer for an O-1A visa, provided the entity is operational and there is a legitimate employer-employee or agency relationship. Many Germany-based professionals pursue O-1A status through their own U.S. company while the EB-2 NIW I-140 processes. For a comparison of the two pathways, see the EB-2 NIW vs. O-1 guide for German professionals.

Not necessarily. USCIS looks for operational substance and legitimate economic activity rather than profitability alone. Early-stage companies with documented clients, expenses, and commercial transactions can support a strong petition. However, a company with no revenue, no clients, and no operational activity adds little evidential value and may raise questions about the applicant's positioning under Prong 3.

Address: 4 W 4th Ave, San Mateo, CA 94402, United States

Email: info@beyondborderglobal.com