H-1B visa holders can buy a house in the U.S. There is no U.S. immigration rule that prevents an H-1B worker from purchasing property. You do not need to be a U.S. citizen or green card holder to own a home.

The more important question is whether you can qualify for financing and whether buying makes sense for your immigration situation. An H-1B worker may be earning a strong salary, living in the U.S. full-time, and planning to stay long term. But the H-1B visa is still tied to employment, sponsorship, extensions, and lawful status. That makes home buying more complicated than it is for a U.S. citizen.

This H-1B Mortgage Guide explains both sides of the decision. On the mortgage side, lenders want to know whether you can repay the loan. On the immigration side, you need to understand what could happen if your job changes, your extension is delayed, your green card process stalls, or your H-1B status becomes uncertain.

Buying a home can be a smart long-term move for some H-1B professionals. But it should not be treated as a simple financial decision alone. Your immigration timeline matters.

Buying a home does not directly help your H-1B visa case. H-1B approval is based on the job, employer sponsorship, wage compliance, and your qualifications for the role.

Home ownership also does not automatically strengthen a green card petition. For EB-1A, EB-2 NIW, or employer-sponsored green card cases, USCIS focuses on professional achievements, eligibility, evidence quality, and the legal standard for that category.

A home purchase may show long-term financial ties to the U.S., but it does not prove visa or green card eligibility. If you are considering a mortgage, it is also a good time to review your long-term immigration strategy.

If you are thinking long term, this is also a good time to review whether an EB-1A green card, EB-2 NIW green card, or employer-sponsored green card route fits your profile.

Yes, many H-1B visa holders can get a mortgage in the U.S. if they meet lender requirements. Mortgage approval is handled by banks, credit unions, mortgage companies, and underwriters, not USCIS.

For mortgage purposes, H-1B workers are generally treated as lawful non-permanent residents. Lenders may approve them if they can show valid legal presence, stable employment, reliable income, credit history, and ability to repay the loan.

Fannie Mae and Freddie Mac guidelines allow eligible lawful non-permanent residents to qualify for conventional mortgages under the same general terms available to U.S. citizens. However, lender rules and documentation requirements can still vary.

Approval is not automatic. Some lenders may ask for more documents, longer visa validity, stronger cash reserves, or proof of continued employment. H-1B borrowers should work with lenders familiar with non-permanent resident mortgage files.

The most common mortgage route for qualified H-1B workers is a conventional loan. Conventional loans are not directly insured by the federal government. Many are underwritten according to Fannie Mae or Freddie Mac guidelines, which may allow eligible lawful non-permanent residents.

This can be useful for H-1B workers with stable employment, strong income, good credit, and enough savings for a down payment. However, lender overlays matter. Even if broad guidelines allow non-permanent residents, a specific lender may apply stricter internal rules.

FHA loans require more caution in 2026. In March 2025, HUD issued Mortgagee Letter 2025-09, which revised FHA residency requirements and removed FHA eligibility for non-permanent resident borrowers for FHA-insured financing, with required implementation for case numbers assigned on or after May 25, 2025.

Since H-1B workers are generally non-permanent residents unless they also have a green card, many H-1B borrowers should not assume FHA financing is available.

Some H-1B borrowers may also consider portfolio loans or non-QM loans. These are loans held by lenders or offered outside standard agency guidelines.

They may be useful for borrowers with unusual documentation, limited U.S. credit history, or special financial circumstances. However, they can come with higher interest rates, larger down payment requirements, and stricter cash reserve expectations.

High-income professionals, such as doctors, dentists, researchers, and executives, may also find specialized professional loan programs.

These programs vary widely by lender and visa status, so H-1B borrowers should review the eligibility rules carefully before relying on them.

Lenders usually want to confirm three things: your identity, your legal ability to live and work in the U.S., and your ability to repay the mortgage.

For H-1B borrowers, this often means providing a valid passport, H-1B approval notice, I-94 record, Social Security number, employment verification letter, recent pay stubs, W-2s, tax returns, bank statements, and credit history.

Some lenders may also ask for your visa stamp, especially if it is relevant to your travel or status history.

Employment stability is especially important. The H-1B visa is employer-specific, so your job is not just a financial issue. It is also connected to your lawful status.

A lender may want to know whether your role is full-time, whether your income is stable, whether your employer is reputable, and whether your H-1B is close to expiration.

Credit history also matters. Many H-1B professionals have strong salaries but relatively short U.S. credit histories.

If you recently moved to the U.S., you may need time to build a stronger credit profile before applying. A higher credit score can improve approval chances and loan pricing.

Debt-to-income ratio is another major factor. This compares your monthly debt payments with your gross monthly income.

Student loans, car loans, credit cards, personal loans, and the proposed mortgage payment can all affect approval.

Down payment and cash reserves can also influence the result. A larger down payment may reduce lender risk.

Strong emergency savings can also matter because H-1B workers face unique job-loss and status-related risks.

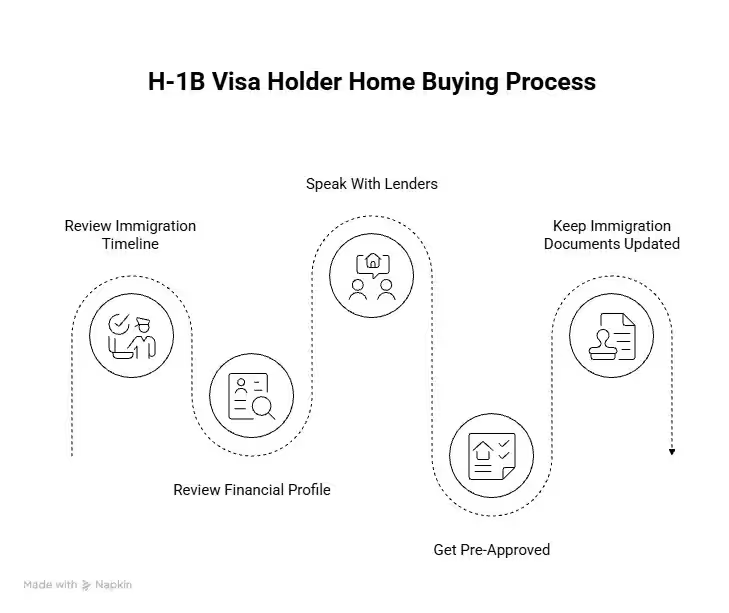

Before applying for an H-1B mortgage, organize your immigration, employment, and financial records. A clean file can reduce delays and help the lender understand your situation.

This is where many generic mortgage articles fall short. For H-1B workers, the risk is not only whether the mortgage is approved. The bigger issue is whether you can safely carry a long-term mortgage while your immigration status depends on employment.

If you lose your H-1B job after buying a home, you may face both financial and immigration pressure.

You may need to find another sponsoring employer, transfer your H-1B, change status, or leave the U.S. If you cannot keep paying the mortgage, you may need to sell the property or rent it out quickly.

If your H-1B extension is pending, you may still be able to apply for a mortgage, but the lender may ask questions.

They may want proof of the pending extension, continued employment, and lawful work authorization. If your current approval is close to expiration, underwriting may become more difficult.

If you are changing employers, timing matters even more. An H-1B transfer can support a job move, but buying a home during a pending transfer may create uncertainty.

From the lender’s perspective, your employment is in transition. From an immigration perspective, your status depends on proper filing and continuity.

If you are already in the green card process, review where you stand.

An approved I-140 may give some H-1B workers more long-term stability, especially for extensions beyond the standard H-1B period. But an approved I-140 is not the same as a green card.

Priority dates, visa backlogs, job changes, and adjustment of status timing can still affect your future plans.

There is no one-size-fits-all answer. Some H-1B workers buy homes before getting green cards, while others wait because their job, location, or immigration timeline is still uncertain.

Buying may make sense if you have stable H-1B employment, strong savings, employer support, a clear green card plan, and plans to stay in the same city for several years.

Waiting may be smarter if your H-1B is close to expiration, your job is unstable, your employer has not started the green card process, or the down payment would use most of your savings.

A mortgage is a long-term commitment. Before buying, make sure your immigration plan is strong enough to support that decision.

Before taking on a long-term mortgage, H-1B workers should understand their green card path, especially if they may qualify for EB-1A or EB-2 NIW instead of relying only on employer sponsorship.

For some H-1B workers, the O-1 visa may be worth reviewing before buying a home, especially if their H-1B job is unstable, their employer may not sponsor a green card, or their H-1B max-out date is approaching. The O-1 is not a mortgage tool, but it can offer another work visa path for qualified founders, researchers, executives, engineers, artists, and other professionals with strong evidence of recognition. Before taking on a long-term mortgage, H-1B workers should understand whether O-1, EB-1A, or EB-2 NIW may fit their long-term immigration plan.

If you are serious about buying a home, you should also be serious about your long-term immigration path.

For some H-1B workers, the employer-sponsored green card process may be the main route. For others, especially founders, researchers, executives, engineers, scientists, and high-achieving professionals, an EB-1A green card or EB-2 NIW may also be worth reviewing.

The reason is simple. A mortgage assumes stability. H-1B status can be stable, but it is still employer-linked and time-limited. A green card strategy can reduce long-term uncertainty if it is realistic and started early enough.

This does not mean every H-1B homeowner needs EB-1A or EB-2 NIW. It means you should understand your options before making a major financial commitment. If your H-1B max-out date is approaching, if your PERM process is delayed, or if you are from a country with long green card backlogs, your home-buying decision should account for that reality.

Start by checking your H-1B approval notice, I-94, extension deadline, employer stability, and green card progress.

If you are planning a job change, H-1B extension, or international travel, consider whether it is the right time to apply for a mortgage.

Next, check your credit score, monthly debts, savings, emergency fund, and down payment.

Do not rely only on your salary. A high income does not automatically mean the mortgage is safe.

Then speak with lenders that understand work visa borrowers.

Ask whether they work with H-1B applicants, what documents they need, whether they accept non-permanent resident borrowers, and whether they follow conventional loan guidelines.

Once you find a suitable lender, get pre-approved before shopping seriously.

Pre-approval helps you understand your budget and shows sellers that you are a serious buyer.

Before closing, keep your immigration documents updated and accessible.

If your H-1B extension, transfer, or green card filing changes during the mortgage process, tell your lender and immigration attorney. Surprises near closing can create delays.

If you are planning a major financial move in the U.S., do not treat immigration as an afterthought. A strong visa and green card plan can help you make better long-term decisions.

Schedule your free consultation and profile evaluation.

Yes. H-1B visa holders can legally buy a house in the U.S. You do not need to be a U.S. citizen or green card holder to own property. However, home ownership does not give you immigration status or protect your H-1B if your employment changes.

Yes. Many H-1B visa holders can qualify for a mortgage if they meet lender requirements for lawful status, income, employment, credit history, down payment, and debt-to-income ratio. Approval depends on the lender, loan type, and the strength of the borrower’s file.

No. A green card is not always required to get a mortgage. Some lawful non-permanent residents, including eligible H-1B workers, may qualify for conventional loans. However, having permanent residence may make underwriting easier with some lenders.

Many H-1B borrowers should not assume FHA loans are available in 2026. HUD changed FHA residency rules in 2025 and removed eligibility for non-permanent resident borrowers for FHA-insured financing. H-1B workers should confirm current eligibility with their lender before relying on FHA financing.

No. Buying a home does not help you qualify for H-1B status. H-1B approval depends on the job, employer, specialty occupation, wage requirements, and your qualifications. Property ownership is not a substitute for valid immigration status.

Usually, no. A home purchase may show financial ties to the U.S., but it does not prove eligibility for EB-1A, EB-2 NIW, PERM, or other employment-based green card categories. Green card evidence should focus on the legal standard for the category you are applying under.

Possibly. Some lenders may consider borrowers with pending H-1B extensions, but they may request extra documentation. You may need to show current employment, timely filing, continued work authorization, and proof that your status remains valid under applicable rules.

It depends on your job stability, savings, H-1B timeline, and long-term immigration plan. If your employer-sponsored green card process is uncertain or your H-1B max-out date is approaching, review your immigration options before taking on a long-term mortgage.

Address: 4 W 4th Ave, San Mateo, CA 94402, United States

Email: info@beyondborderglobal.com