U.S. long term visa, entity and bank account setup, fully managed.

.png)

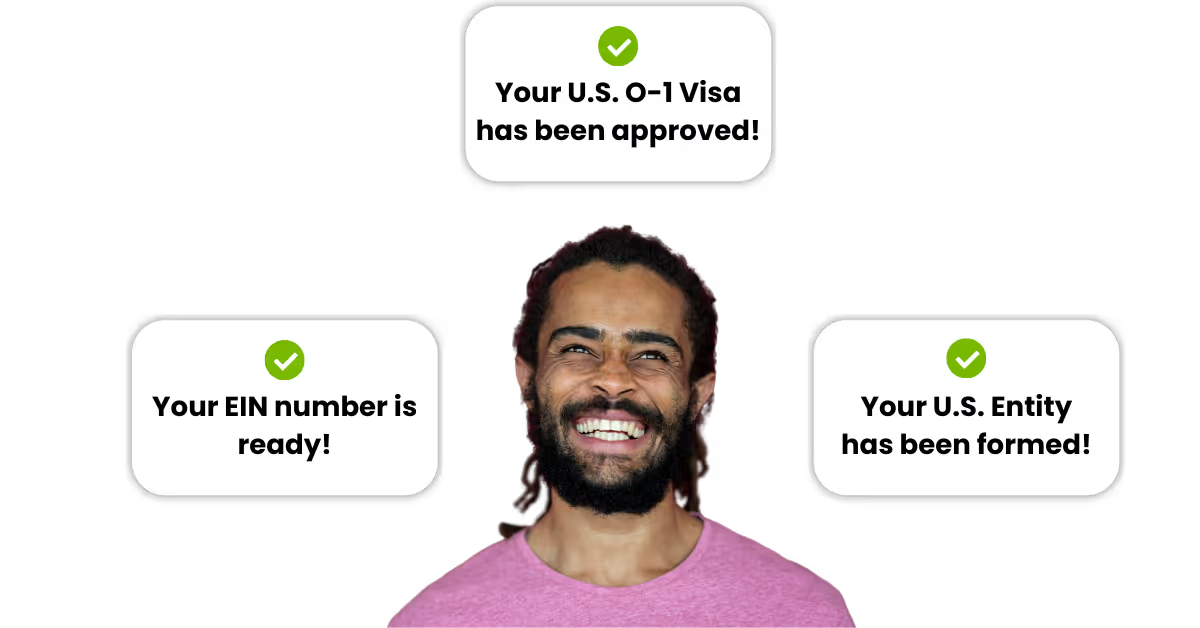

Manage all your U.S. launch's corporate needs with our all-in-one offering.

.png)

.png)

-min.webp)

We pre-vet our attorneys with strong track records, so you don’t have waste months finding a good one.

Founders and Launch Teams trust us to handle their US expansion needs, a one stop go to solution.

Work with 15+ years of combined extraordinary visa knowledge. We are confident in your approval.

We guarantee to complete the petition drafting and submission within 1 month of receiving all supporting documents required to file your long term visa or green card petition. Beyond Border is amongst the fastest legal service provider in the industry, thanks to our tech-enabled approach to petition filing and focus on technologists.

The fee will vary depending on the visa or green card type that best suits your need, but you should budget between US$8,000-10,000, excluding government fees and depending on your long term visa or green card category.

You can visit USCIS's free fee calculator to get an estimate for the associated government fees to process your visa.

Beyond Border is a modern immigration platform founded by immigrants from the technology industry for immigrants. We leverage technology to speed up the end-to-end U.S. immigration petition process, and work with a carefully curated network of attorneys who specialize in U.S. immigration cases for technologists.

Our attorneys maintain a 98% success rate throughout their careers with more than 4,000 approvals. We work exclusively with venture backed tech operators and researchers, which allow us maintain a high approval rate and provide profile building advice given sector expertise.

If your application is rejected, we will review the reasons for denial and help you reapply by addressing any issues or missing documentation.